USAID. MISSION TO EGYPT

USAID public finance administration project (263-0209)

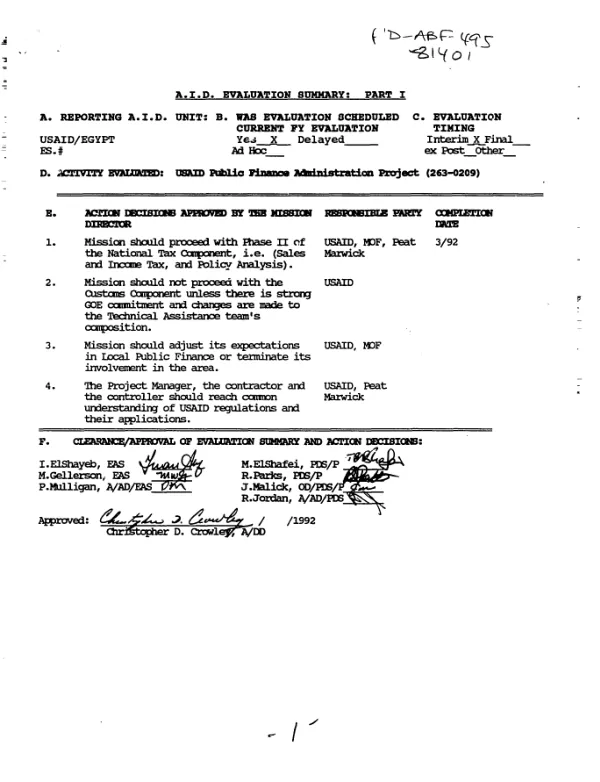

Summarizes two evaluations (PD-ABE-184 and PD-ABE-204) of Phase I of a project to improve the efficiency and equity of tax administration in Egypt.

1970

Sign in to readA free account is required to download.

Abstract

The evaluations covered the period 11/87-6/92 and focused on project components concerning (1) national tax, (2) local finance, and (3) customs. The national tax component has proceeded extremely well, although not according to the original schedule. Phase I was largely devoted to redrafting legislation, preparing forms, training employees, and generally gearing the Ministry of Finance (MOF) up to implement a sales tax to which the Government of Egypt (GOE) had committed itself under an IMF agreement. The key product of these efforts was a document entitled "A Comprehensive Tax Reform Program for Egypt," which reflects the best current thinking on tax systems. As a result of this emphasis on sales tax, work in the income tax area is still in the early stages, and much remains to be done in Phase II to implement a global income tax. Work in local finance was more disappointing. While contractual obligations were met, results were meager. The problems seemed to stem from differing USAID and GOE expectations and the GOE"s failure to include the MOF as an integral counterpart. Further activity in this area should be based on more realistic USAID expectations and demonstrated GOE commitment. From the outset of the customs component, the U.S. Customs Service PASA team encountered difficulties stemming from the lack of the Egyptian Customs Authority"s (ECA) commitment to the project and from the team"s inability to deal with USAID requirements regarding training, procurement, and work plans. Either the PASA should be altered in terms of team composition, or the project should be continued under a different contractor. In either case, the ECA and the MOF need to indicate a positive commitment to the project. It is recommended that the Mission proceed to Phase II with the sales tax, income tax, and policy analysis components of the project and reinforce its efforts to ensure that a policy analysis unit is established in the MOF. This should be the highest priority. Experience with the sales tax activity of the national tax component teaches that external circumstances can create a positive environment where none existed before. The success of this component can be attributed to the support of the Minister of Finance, a highly competent TA team, and most importantly the various pressures created by the Gulf War and subsequent negotiations with the IMF.

Related documents

![Local development II [LD II], 263-0182](https://covers.devme.ai/gen/36480.webp)