USAID. BUR. FOR GLOBAL PROGRAMS, FIELD SUPPORT AND RESEARCH. CENTER FOR ECONOMIC GROWTH. OFC. OF ECONOMIC AND INSTITUTIONAL REFORM

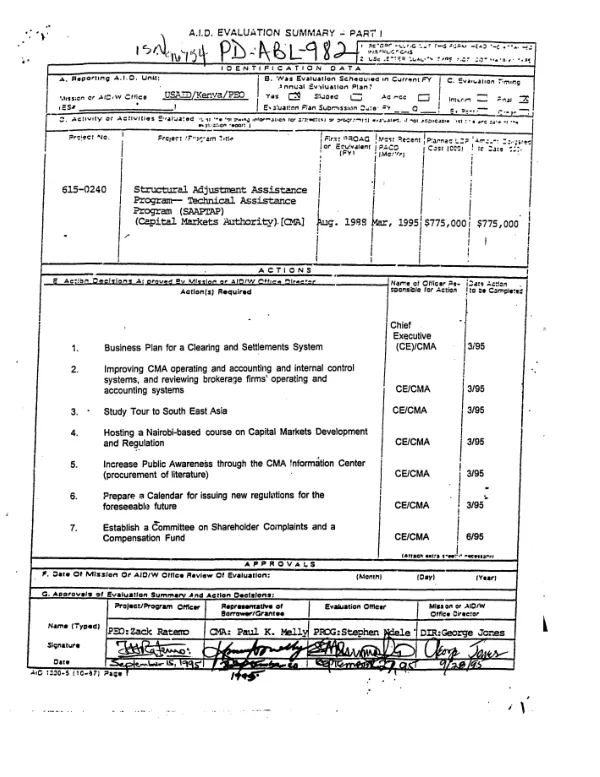

Final report -- Kenya : evaluation of Capital Markets Authority

Final evaluation of a project component (8/88-9/94) to help to develop Kenya's capital markets, in particular the Kenyan Capital Markets Authority (CMA) and the Nairobi Stock Exchange (NSE).

1994

Sign in to readA free account is required to download.

Abstract

Accomplishments have been remarkable given the project's relatively short life and the adverse economic, financial, and political context within which it has had to operate. A reasonably well-formed and functioning, though embryonic, capital market is in place. The CMA and NSE have essentially been built from the ground up and are firmly established; the CMA has developed and is enforcing rules and regulations governing capital markets and the NSE, and the NSE has demonstrated impressive growth in terms of outstanding shares, trading volume, and market index. The Government of Kenya has lived up to its part by enacting the Securities Act and taking other steps to facilitate the expansion of capital markets. The outlook for sustainable, steady growth in the Kenyan capital market is good. However, it would be prudent to think of the Kenyan capital market as still being in its infancy and in need of nurturing, rather than on the verge of joining strong emerging markets such as Thailand and Indonesia. A number of concerns remain, however. (1) Capital markets revolve around three core institutions: the regulatory authority, stock exchange, and clearing and settlement facility. While the first two have been addressed under the project, clearing and settlement seem to be the "forgotten child." The CMA and USAID advisors need to turn their attention to development of a formal system for clearing, settlement, and registration. (2) While the growth of the NSE has been promising, liquidity (an overall measure of trading activity) is still quite low. Stepped up efforts are needed to attract more listed companies to the market and to promote the stock exchange among investors. (3) Political factors are a concern: local political conflicts have the potential to spill over into and slow the capital markets development process; and the roles and responsibilities of the CMA vis-a-vis the NSE, and of these two newer institutions vis-a-vis existing government agencies, are still in flux, causing considerable organizational conflict. The project can continue to assist the CMA and NSE by improving their organizational structures, the Securities Act and particular regulations, and market liquidity. The project has shown that (1) capital markets can be developed under adverse economic and political circumstances, and the process can be quite rapid, (2) even embryonic, relatively unstructured markets can play an effective role in mobilizing savings and allocating capital, (3) transfer of knowledge and expertise is feasible in the field of capital markets development, and (4) an effective capital markets assistance program does not have to be particularly expensive or comprehensive. The project has also confirmed a number of negative findings from other, similar efforts: (1) establishing effective capital markets regulation and a culture of compliance can take quite a while, (2) during their emerging phase, capital markets are subject to local political conflicts which can slow progress or arrest it altogether, and (3) clearing and settlement is often the "forgotten orphan" in capital markets development programs.