USAID DEC

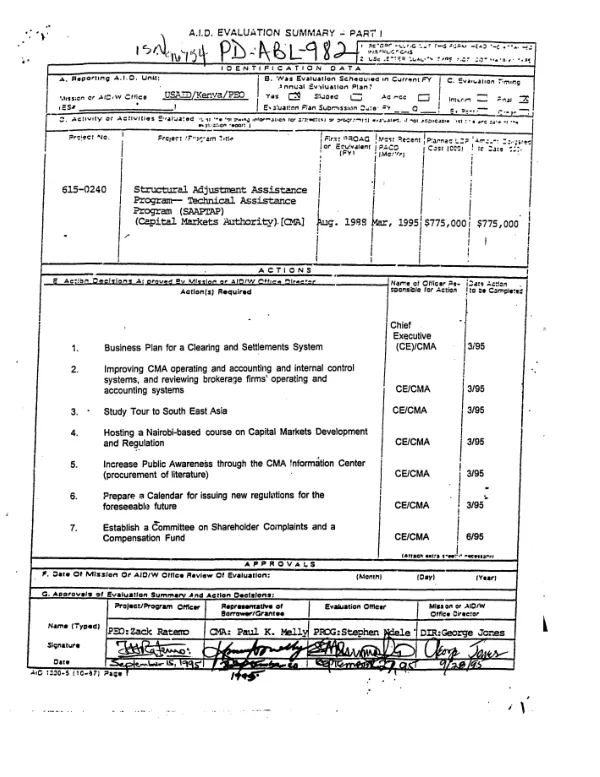

Structural adjustment assistance program -- technical assistance program (SAAPTAP) (Capital Markets Authority (CMA))

Sign inUSAID. MISSION TO KENYA

Structural adjustment assistance program -- technical assistance program (SAAPTAP) (Capital Markets Authority (CMA))

Summarizes final evaluation (PD-ABJ-521) of a project component (8/88-9/94) to finance TA for Kenya"s Ministry of Finance in the creation of a functional capital markets development authority.

1995

Sign in to readA free account is required to download.

Abstract

Capital markets did not really exist in Kenya before the initiation of the component. There was neither a Securities Act nor a regulatory agency; the Nairobi Stock Exchange was a private association whose six members did not trade among themselves and could not be termed a "stock market" in the accepted sense of that term. Overall, it can be concluded that a reasonably well-formed and functioning, if still embryonic, capital market has been implemented in Kenya over a remarkably short period, and in a very adverse economic, financial, and political context. That market is capable of sustained growth. It can also be concluded that the assistance provided by the component has been critical to both the quality and the timeliness of this development, which would likely have been placed in serious jeopardy if the assistance had not been available. Capital markets center around three core institutions: the regulatory authority (the Capital Markets Authority -- CMA), the stock exchange (NSE), and the clearing and settlement facility. During the USAID project, two of these core institutions were built from the ground up in Kenya: the CMA and the NSE. The USAID-funded advisor to the CMA played an important and fruitful role in these developments. Unfortunately, the deterioration of the relationship between the CMA and NSE made the advisor"s position increasingly untenable, eventually forcing him to curtail and then stop his work with the NSE. It is doubtful whether the two institutions have matured sufficiently by now to be left to their own devices with confidence. Key recommendations are to: review the CMA Act and regulations; review CMA lines of authority, operations, and accounting practices; develop a clearing and settlements process; improve internal management of NSE; increase public awareness of rules and regulations of the capital markets; increase listing and trading on the exchange; not financially subsidize the normal operations of the NSE; define and implement "self-regulation" of NSE; and establish a complaints committee and compensation Fund in NSE. A key lesson learned is that capital markets can be developed in most adverse economic, financial, and political circumstances with very little funding, although full development of such markets will take many years. (Author abstract)