USAID. MISSION TO GUATEMALA

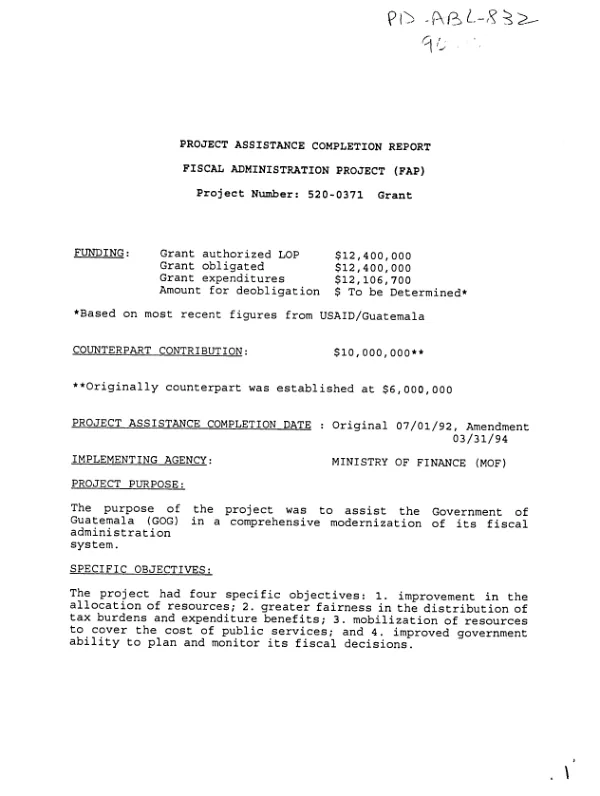

Fiscal administration project (FAP)

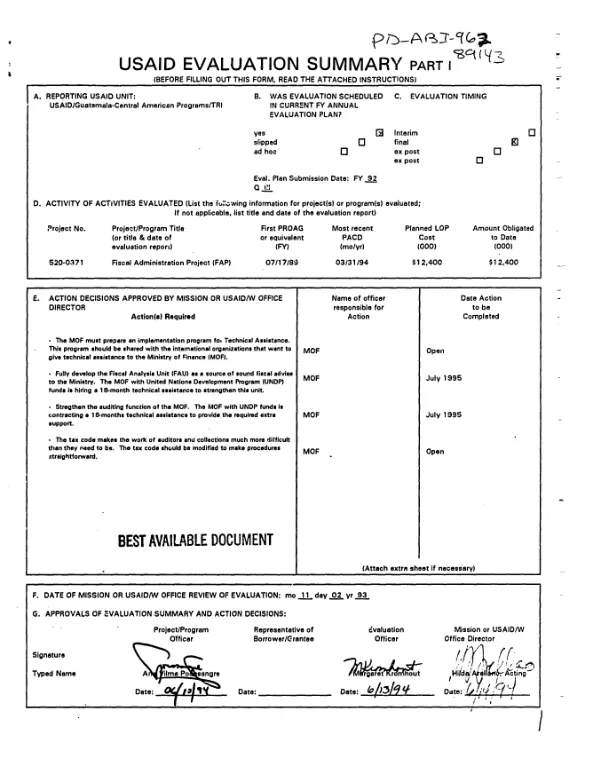

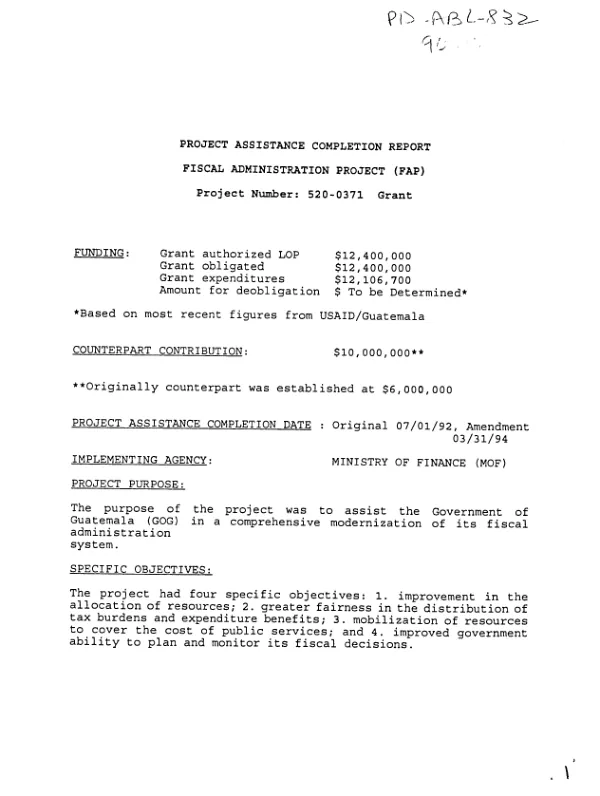

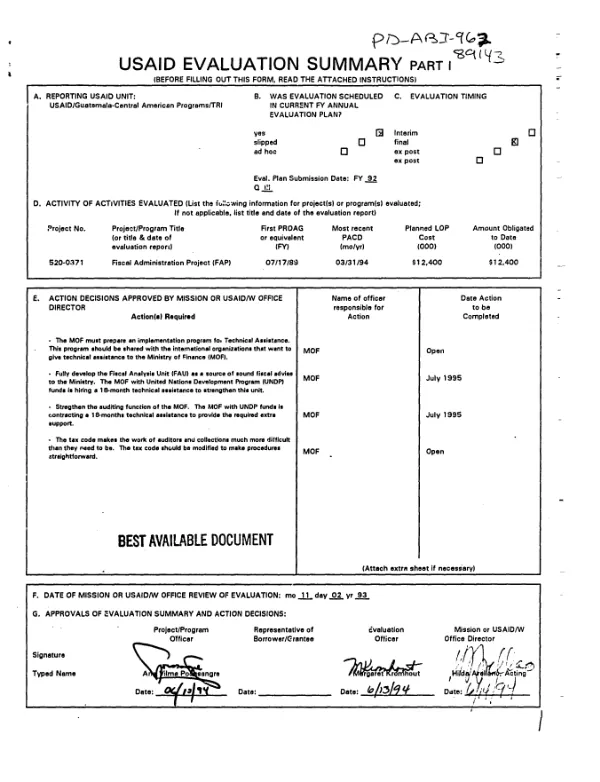

Summarizes attached final evaluation (XD-ABI-962-A) of a project (7/89-3/94) to help Guatemala"s Ministry of Finance (MOF) to modernize its fiscal administration systems, especially in the areas of budgetary management, tax structure analysis, and tax administration.

1994

Sign in to readA free account is required to download.

Abstract

The project achieved most of its original goals; omissions have been few (e.g., activities in budgeting were limited) and several important activities were added during implementation. the most important activity has been the key role played by the TA team in implementation of the tax modernization program, the centerpiece of which is the new tax laws approved by Congress in June 1992. In addition, the MOF"s computerized systems have been modernized; a new department, the Direccion de Analisis Fiscal (FAU), was established to provide assistance to the Minister in fiscal policy formation and management; control systems have been put in place to assist in managing tax-related matters; and training has been conducted in almost all functions of the Internal Revenues Directorate (DGRI) and Customs Directorate (DGA). While there are reasons to be optimistic that the project"s initiatives will be institutionalized within the MOF, the fact is that institutionalization was only partial and remains fragile. On the positive side, there exists a well-trained staff within DGRI"s computer section to continue the project"s initiatives, and commitment at high levels of the MOF remains strong, as evidenced by MOF"s having committed its own resources to follow up on measures suggested or initiated by the project. On the negative side, not all of the MOF"s divisions were modernized; duplication of efforts and/or confusion about responsibilities remain; special contracts, rather than civil service hiring, have been the primary vehicle for upgrading personnel; and much progress has depended on the good will and support of the Minister and Vice Minister. The following areas still need to be addressed: (1) the tax code is very awkward and does not support effective tax administration; (2) tax auditing is still very weak; (3) FAU is not yet fully developed as a source of sound fiscal advice to the MOF; and (4) tax revenues have not increased as they should. Lessons learned included the following. (1) The straightforward design of the project -- which targeted known and agreed-upon problems at the MOF -- contributed to its quick acceptance by the MOF and thus to its success. The MOF was quick to adopt a sense of ownership about the project; was willing to share confidential information with the TA team and to include them in sensitive negotiations; and provided a greater than expected counterpart contribution. However, TA personnel must avoid being drawn into taking responsibility for day-to-day operations of the counterpart organization. (2) The failure to designate a counterpart team at the MOF at the outset was a tremendous oversight. A team should have been in place to immediately begin absorbing knowledge and experience from project consultants, which would have contributed to the continuity and sustainability of the project. (3) The MOF needs to develop its own fiscal strategy in order to get better results in the implementation of its policy.

Related documents