USAID DEC

Housing Development Finance Corporation of India : evaluation of the housing guaranty loan

Sign inUSAID. BUR. FOR PRIVATE ENTERPRISE. OFC. OF HOUSING AND URBAN PROGRAMS

Housing Development Finance Corporation of India : evaluation of the housing guaranty loan

Evaluates Housing Guaranty (HG) to develop the institutional viability of the Housing Development Finance Corporation (HDFC), a private Indian firm.

Buckley, Robert|Khadduri, Jill|Struyk, Raymond · 1985

Sign in to readA free account is required to download.

Abstract

Special evaluation covers FY's 81-84 and is based on document review, site visits, and interviews with USAID/I, World Bank, and HFDC personnel and with consultants. HDFC has substantially increased resource mobilization via deposits, term borrowings, and bonds, and is currently developing new methods based on taking a small equity position in housing finance institutions in underserved areas. By the end of FY 84 HDFC was 150% larger than forecasted; had increased financing through term borrowings from 34% to 42%, against a target of 45%; and had raised 25% more resources in local markets than had been targeted. It has also cautiously avoided unnecessary risk exposure. While HDFC is not likely to achieve the target of directly raising $400 million within 5 years of HG disbursement, this is not necessarily a desirable goal. HDFC has promoted regulatory change, e.g., a shift in the allocation of funds from commercial banks which has enabled the latter to become involved in housing finance. HDFC has also made a good faith effort to develop a policy for low-income applicants and allocated 30% of all its loans to them during FY's 82-84. HDFC is cautiously preparing to initiate a plan in which low-income persons who make deposits over a 2-7 year period at low interest rates will be permitted to borrow at the same rates. HDFC has subsidized a corporate loan program which enables companies to provide quality housing for their workers by making loans both available and affordable. Since this effort directly benefits low-income households, it constitutes an appropriate use of HG funds. The $100,000 in TA has been used for training which has provided a framework for improving nonfinancial management procedures and personnel practices. It is recommended that the HDFC: (1) strongly pursue its policy of expanding its base of individual deposits; and (2) focus on increasing loan affordability through loan term modification and by expanding the supply of market rate mortgage credit.

Related documents

Documents in this collection

USAID DEC

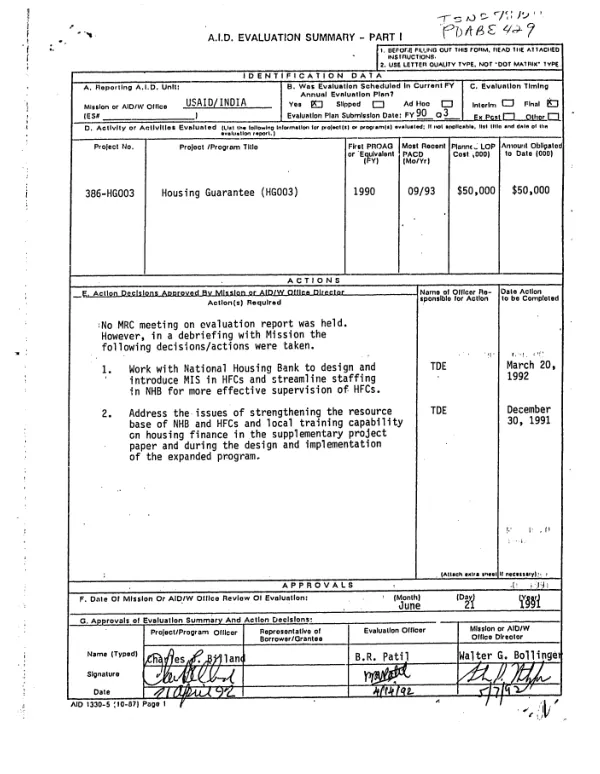

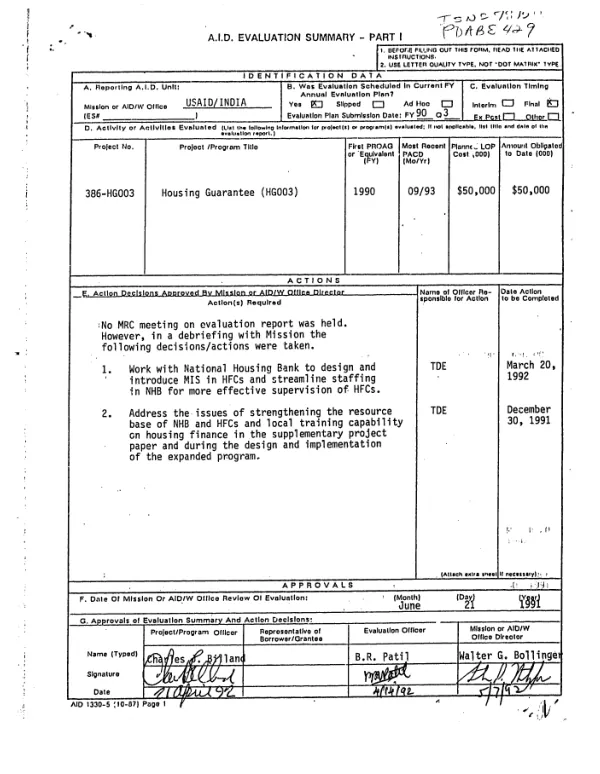

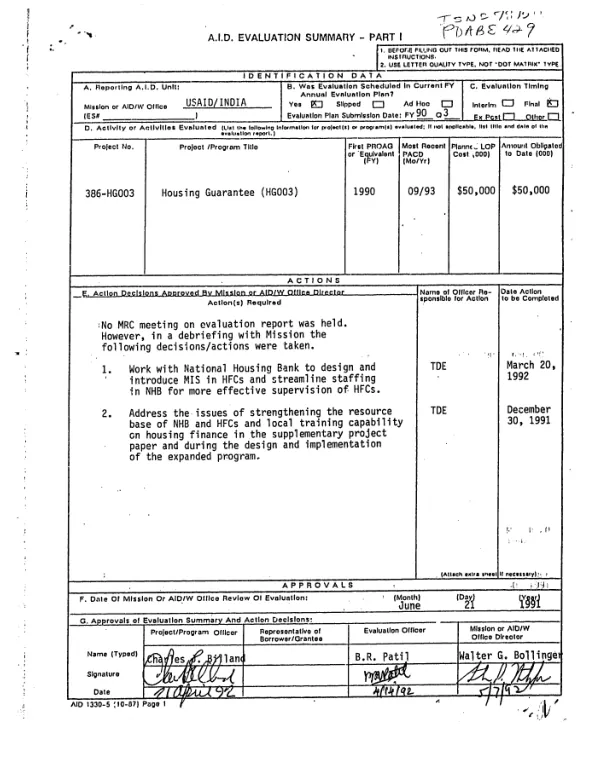

Market-oriented housing finance in India : the National Housing Bank's first two years -- interim evaluation of the HG-003 program

Open record 1970

1970USAID DEC

Market-oriented housing finance in India : the National Housing Bank"s first two years -- interim evaluation of the HG-003 program

Open record