USAID. MISSION TO INDIA

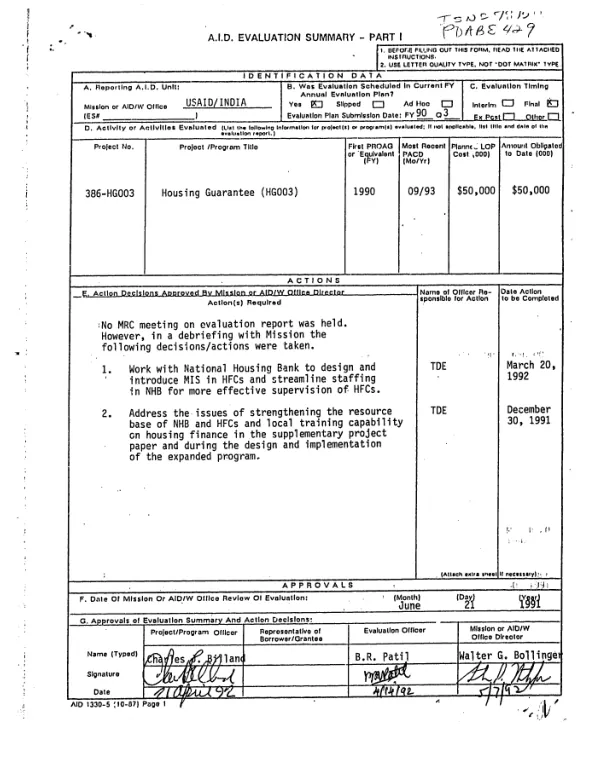

Housing guarantee (HG003)

Summarizes interim evaluation (XD-ABE-429-A) of a Housing Guaranty (HG) program to help India develop a market-oriented system of housing finance companies (HFC"s) to serve low-income households.

1992

Sign in to readA free account is required to download.

Abstract

The evaluation covered the period 8/88-8/91. Overall, the program is meeting its goals. The Housing Finance Company (HFC) network has grown substantially, with the total number of registered HFC"s increasing from about 30 in 1988 to at least 250 in 1991. Sixteen HFC"s have been approved to receive refinancing from the National Housing Bank (NHB) -- a status indicative of maturity -- and two more are in process of being approved. Data from 9 of the largest HFC"s indicate that the number of loans sanctioned by HFC"s grew at a compound annual rate of 44% from 1988-89 to 1990-91; in the final year, these 9 HFC"s sanctioned about 153,524 loans. Overall, the HFC"s have performed well in raising funds, leveraging equity, and reaching a minimum level of profitability. Credit risks on individual loans appears to be low, as do the HFC"s liquidity and capital risks. However, interest rate risk could become a problem in the future. There is also a risk that some private HFC"s may become overly dependent on NHB"s refinancing facility. Available data indicate that one-quarter of HFC borrowers are below-median income households. This represents only a modest increase in share over the past 2 years, but is a substantial achievement, given the explosive growth in total lending by the HFC"s. All HFC"s deny any discrimination against lending to households headed by females or elderly persons, but data were inadequate to verify this claim. Program management has generally been effective. The NHB has been very active in promoting the development of a housing finance system, while USAID has funded substantial complementary training, studies, and TA. However, NHB"s record of supervising HFC"s is poor, especially with regard to HFC"s that are not recognized for refinancing from NHB. NHB"s implicit refinancing commitments are likely to outstrip the resources available from low cost funds allocated by government bodies. Conservative estimates indicate that substantially more than $25 million in loans will be presented each year for refinancing. NHB has therefore begun exploring options for obtaining capital from the market. The primary lesson learned is that new institutions often concentrate on fulfilling certain aspects of their mandate at the expense of others; NHB performed well in industry promotion, but paid insufficient attention to funds mobilization and industry supervision.

Related documents

Documents in this collection

USAID DEC

Market-oriented housing finance in India : the National Housing Bank's first two years -- interim evaluation of the HG-003 program

Open record 1970

1970USAID DEC

Market-oriented housing finance in India : the National Housing Bank"s first two years -- interim evaluation of the HG-003 program

Open record