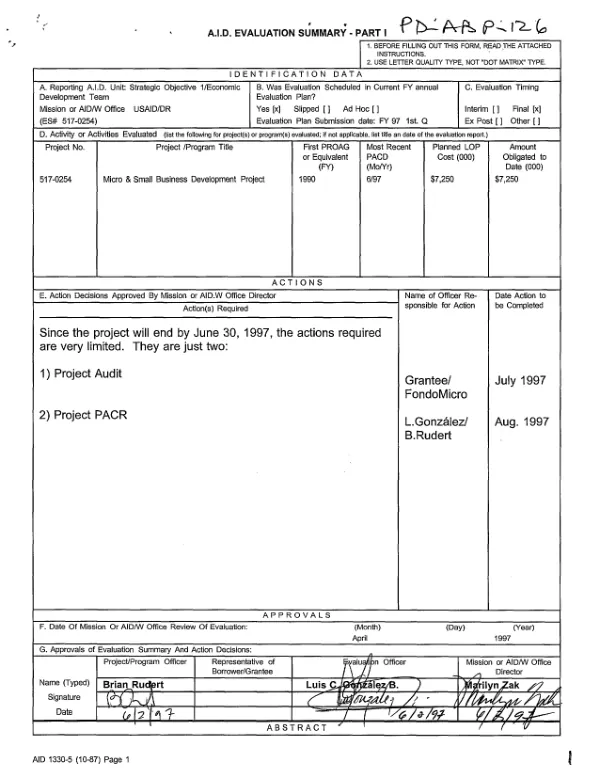

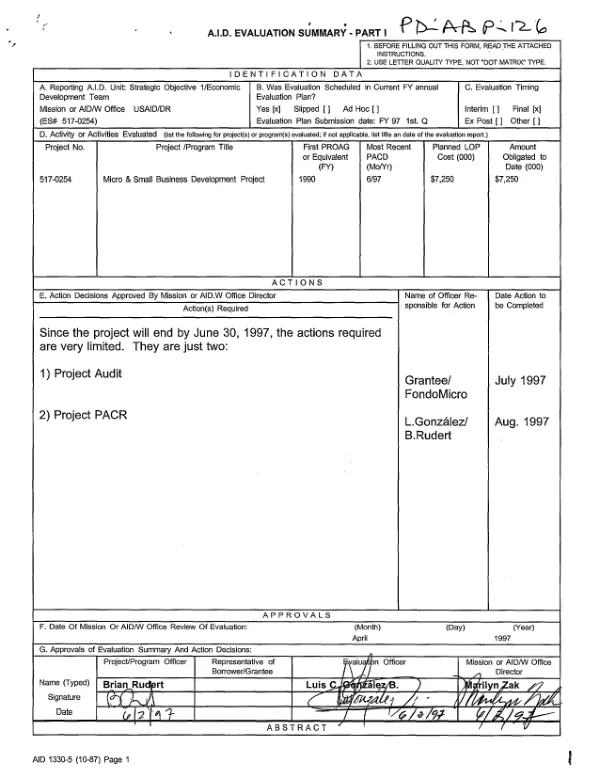

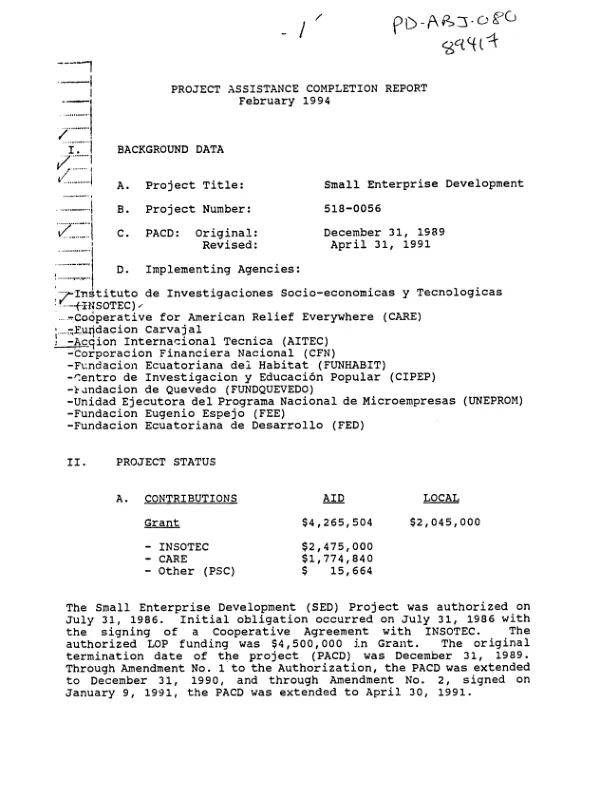

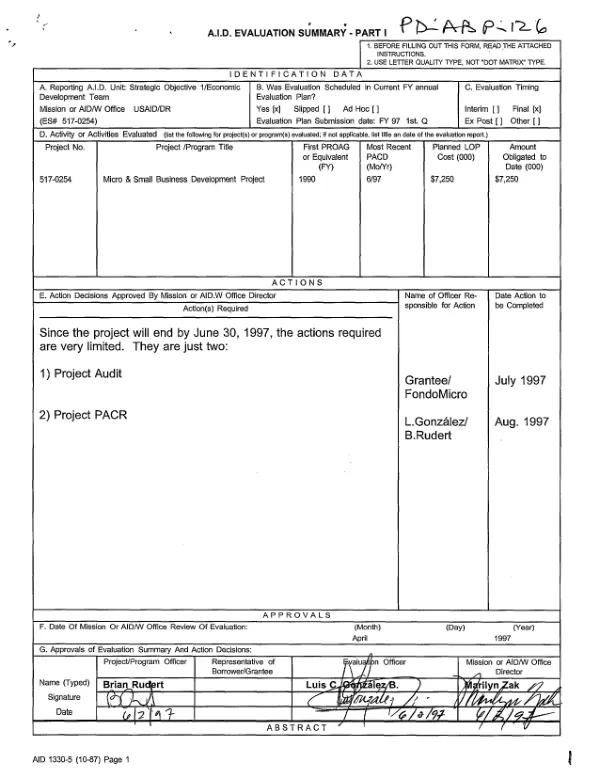

USAID. MISSION TO DOMINICAN REPUBLIC

Micro and small business development project

Summarizes final evaluation (XD-ABP-126-A) of a project (6/90-6/97) to develop the institutional capacity of FondoMicro, a new Dominican NGO, to provide financing and TA to NGOs operating credit programs for the informal small and micro enterprise (ISME) sector.

1997

Sign in to readA free account is required to download.

Abstract

The project failed to reach the large, broad audience of SMEs that was its target (though it achieved a high percentage of female participation in the program), mainly because there were few viable NGOs that qualified, even with intensive TA, to manage the project"s credit resources. As the project neared completion, FondoMicro (with USAID approval) sponsored the creation of a for-profit Small Business Bank, which it believes will more effectively meet ISMEs" credit and savings needs. This will require specific mechanisms to ensure that the Bank does in fact serve the informal microenterprise sector, rather than skew its attention toward the easier to reach small and medium businesses in the formal sector. The credit programs in the five NGOs with active lines of credit from FondoMicro generally appear well managed, though reserves for uncollectible loans seem inadequate and taken together are only about a third of the appropriate level. The project lacked effective leverage to ensure that potential NGO participants would take steps to improve their managerial and organizational capabilities, since many had alternative sources of credit. The lack of a regulatory entity responsible for supervising prudential norms among NGOs further weakens their ability to serve as the basis for a sustainable credit system. The fundamental issues that limit the growth and sustainability of FondoMicro and its clients are high administrative costs in relation to the portfolio size, and the high cost of capital (except when donated). These problems derive from legal provisions that prohibit savings mobilization and full participation in financial intermediation. Given the large unmet demand for credit within the SME sector, and the likely dwindling of donor assistance, which has been the chief source of funds (other than supplier credit), institutions serving the sector must be able to serve as effective links to the capital of net savers within the economy, such as savings and loan cooperatives or private banks. For its part, Fondomicro, whose anticipated role as a clearinghouse for donor assistance to the NGO sector failed to materialize, should prepare and disseminate a targeted strategic plan that demonstrates how it intends to assist the microenterprise sector in the future. It is more important to maintain FondoMicro"s TA function than to maintain its credit function, as it is not a cost-effective provider of credit. The following lessons were learned. (1) Dominican NGOs have structural weaknesses, such as legal prohibition on mobilizing savings deposits and limited access to commercial bank loans, which limit their becoming self-sustaining financial intermediaries that can serve as stable sources of credit for SMEs. (2) A second-tier financing institution can only survive if it has access to resources at rates sufficiently cheap to enable it to generate the margins needed to cover expenses. Careful financial planning is required before promoting creation of a second-tier organization to ensure that there is an economic niche for it. (3) Microenterprises are able and willing to pay extremely high interest rates for short periods of time, but these rates probably mask inefficiencies in the NGOs that serve as credit channels. (4) The microenterprise sector is quite diverse. It is commonly assumed that loans to microenterprises quickly translate into increased employment (the goal of this project). However, FondoMicro"s experience has shown that over half of Dominican microenterprises exist at a subsistence level, where increased incomes are immediately used to improve family living standards rather than to hire more employees. In addition, loans to microenterprises in the commerce and service sectors generate fewer new jobs than do loans to the manufacturing sector; the latter, however, requires longer-term financing, often in higher amounts, than do the other sectors. Depending on program objectives, USAID may need to more narrowly focus its assistance on microenterprise subsectors.

Related documents