USAID

Revenue Mobilization in Haiti

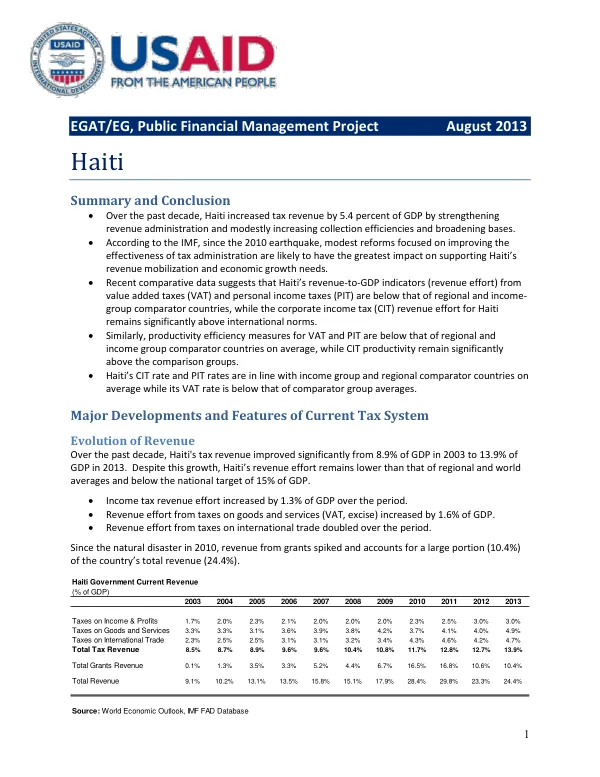

Over the past decade, Haiti has made significant progress in strengthening its revenue administration and increasing tax revenue.

2013 · 5 pages

Sign in to readA free account is required to download.

Abstract

The country's tax revenue has grown from 8.9% of GDP in 2003 to 13.9% of GDP in 2013. This growth is attributed to modest reforms focused on improving the effectiveness of tax administration, which are likely to have the greatest impact on supporting Haiti's revenue mobilization and economic growth needs. Haiti's revenue effort remains lower than that of regional and world averages, and below the national target of 15% of GDP. The country's overall tax revenue, at 12.8% of GDP, is in line with the selected sample group, slightly below the average for income group comparator countries, and significantly below the averages for the CARICOM region, the LAC region, and the world. Haiti's revenue effort from personal income tax is 2.5% of GDP, which is modestly below the income group average and almost half that of the regional and world averages. The corporate income tax revenue effort for Haiti, at 7.9% of GDP, is more than twice the average of the selected sample group and income group, and significantly above the averages for the CARICOM region, the LAC region, and the world. The revenue effort from VAT, at 3.2% of GDP, is considerably below that of the sample group and income group comparator countries, and nearly half that of the CARICOM, LAC, and world averages. Haiti's tax structure is characterized by a corporate income tax rate of 30%, which is slightly above the income group and regional averages, and modestly above the world average. The maximum PIT rate in Haiti, at 30%, is in-line with the world averages and its sample group, income group, and regional comparator countries. The VAT rate, at 10%, is 5 percentage points below its sample group comparator averages and significantly below the rate of its direct neighbor, the Dominican Republic. Revenue productivity measures the revenue share of GDP that is mobilized for each point of the tax rate. Haiti's corporate income tax productivity, at 0.26, is nearly triple the amount of the selected sample group and income group comparator countries, and significantly above the LAC and CARICOM regional and world averages. Personal income tax productivity, at 0.08, is modestly below that the selected sample group average, and considerably below the income group, LAC, and CARICOM regional averages. The Haitian authorities have adopted a ten-year action plan for building a better Haiti, which includes substantial debt relief and the 2010 signing of the IMF Extended Credit Facility Agreement. Tax reforms since the 2010 natural disaster include the establishment of two new taxes, import tariff reform, ongoing reforms to attribute larger powers to the revenue collections agencies, increased focus on combating fraud and tax evasion, and increased targeted taxes on tobacco, alcohol, and gambling. Administrative measures include draft legislation to reorganize the DGI along functional lines, the launch of the e-declaration, the establishment of the Unit for the Analysis of Fiscal Policy, and the introduction of Medium-Size and NGO Taxpayer Units. Efforts to strengthen tax and customs administration, reduce and rationalize exemptions, and expand the tax base will take time to show results in the current environment. An increase of the VAT rate from 10% to the regional (LAC) average of 13.5% would yield additional revenue of about 1 percent of GDP. If personal income tax productivity were to reach the level of the selected sample group average, Haiti would yield an additional 0.75 percent of GDP of revenue. If VAT productivity were to reach the level of LAC and CARICOM regional averages, Haiti would yield an additional 0.50 percent of GDP of revenue.