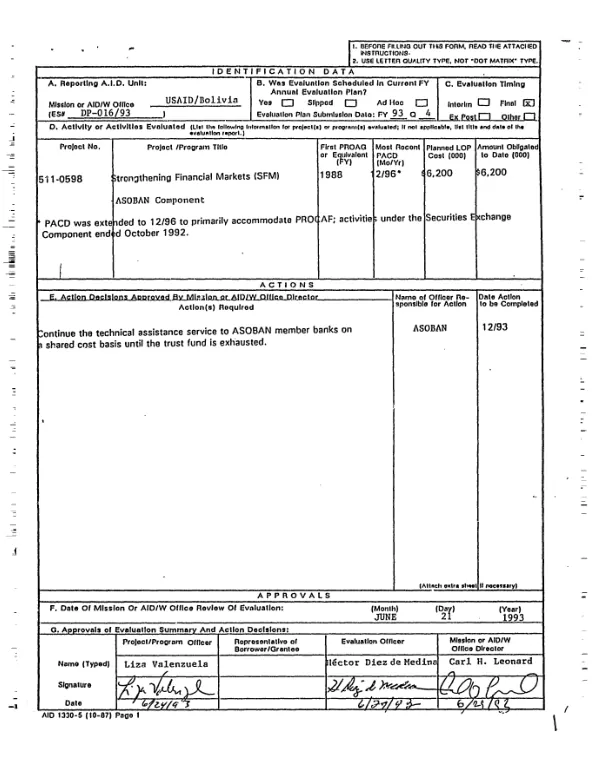

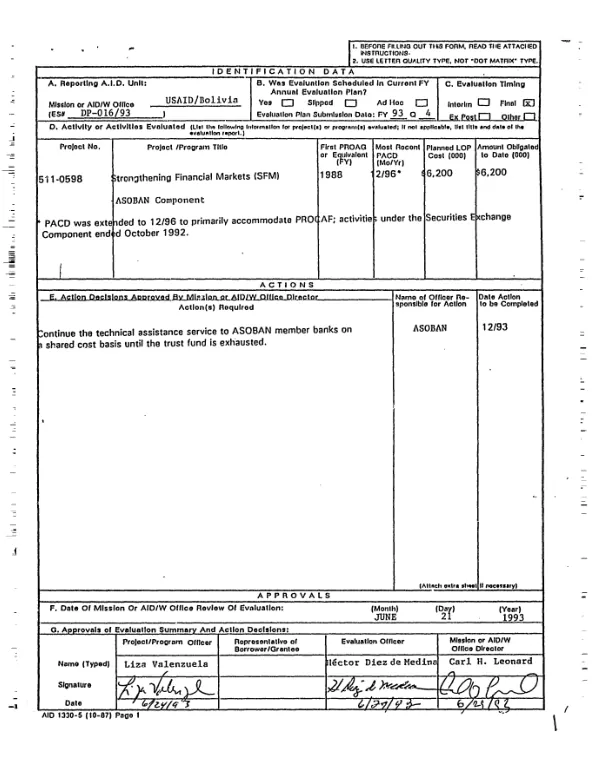

USAID. MISSION TO BOLIVIA

Strengthening financial markets (SFM) : ASOBAN component

Summarizes attached final evaluation (XD-ABG-398-A) of efforts to strengthen the Association of Banks and Financial Institutions of Bolivia (ASOBAN) as part of a project to strengthen Bolivia"s financial sector.

1993

Sign in to readA free account is required to download.

Abstract

The evaluation covered the period 9/89-6/93 and focused on four ASOBAN activities: (1) TA consultancies offered to member banks; (2) economic and legal analysis services; (3) a check clearing facility; and (4) a computerized central information system for credit referral. Over the life of the project, ASOBAN carried out 12 TA consultancies at 8 commercial banks. Of the 12, 8 were considered adequate by the banks and were paid for by the project (consultants are paid in full by the project, and banks are billed 50% of the costs, which amount is paid into a trust fund so that the service can continue when the project is over). The other 4 consultancies, all in the area of marketing, were considered inadequate by both the banks and Nathan Associates, the institutional contractor, and were not paid for. ASOBAN did not market this service in 1993, as its staff were involved in development of Bolivia"s new banking law. However, there is a demand for the service, and ASOBAN should draw up plans for continuing it. ASOBAN is providing its member banks with economic analysis generated by an in-house unit staffed by two professionals, and legal analysis, provided primarily by an outside lawyer who works as a consultant. ASOBAN"s legal analysis contributed significantly to the new banking law. ASOBAN also represents commercial banks in the negotiation of nationwide contracts for the sector. In 12/92, ASOBAN facility took over operation of most of the country"s check clearing system from the Central Bank. The system is operating smoothly and all commercial banks participate. The clearing system is still primarily manual, but automating it would not be cost effective, since the volume of checks cleared daily in Bolivia is small. By the time ASOBAN"s central credit referral information system was ready to operate in 11/91, a similar system had been in operation by the Superintendency of Banks had for 7 months. In addition to the redundancy, ASOBAN"s data base includes only clients active at the beginning of 1991, and was obsolete by the time it was installed. Expenditures made thus far should be written off. However, 90% of bankers interviewed saw a need for a private credit referral system which would offer supplementary information to that offered by the Superintendency and be more timely. At least one private firm has begun to offer these services; ASOBAN should watch its progress and allow the market to determine whether a more sophisticated system is necessary. Lessons learned include the following. (1) There is clearly a demand for short-term consultancies, but they need to be tailored more carefully to clients" needs, and client banks should check the references of proposed consultants. (2) ASOBAN"s input into the new Bolivian banking law demonstrates that banking associations can have substantive impact on the legal and regulatory environment in which banks operate. (3) The failure of ASOBAN"s central information system was the result of poor communication between the system"s developers, the Superintendency, and ASOBAN member banks.