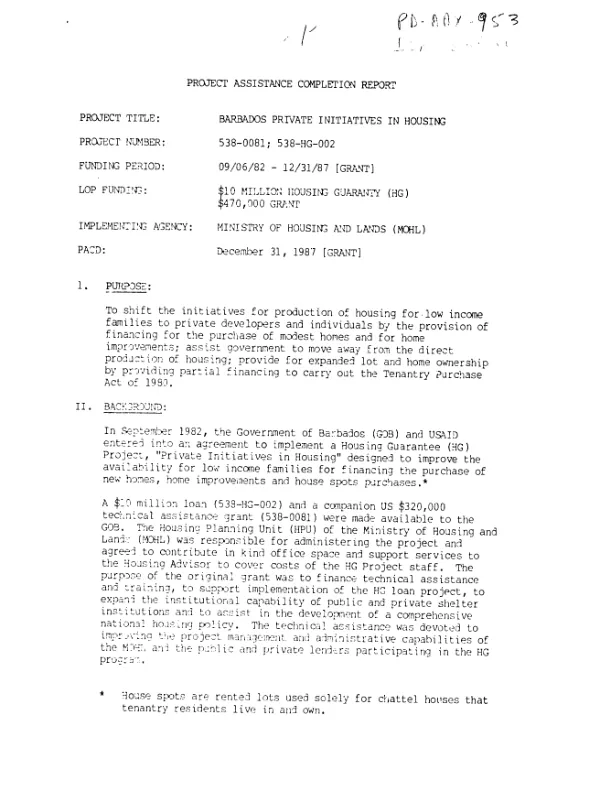

BARBADOS. MINISTRY OF HOUSING AND LANDS

Barbados private initiatives in housing

Final Mission report on a Housing Guaranty (HG) loan and companion grant (9/82-12/87) to promote private sector initiative in producing low-cost housing in Barbados.

1987

Sign in to readA free account is required to download.

Abstract

The project significantly expanded financing to lower-income borrowers. Repayment rates have been good. (1) The mortgage component made 237 loans - 143 totaling $4.2 million from HG funds and 94 totaling $4.4 million from loan reflows. HG funds were lent through the Barbados Mortgage Finance Company (BMFC) and Caribbean Commercial Trust. (2) The home improvement (HI) program used commercial banks and credit unions to make 3,407 loans worth $6.2 million. The program's large scale and the positive attitude of borrowers (who represented a broad cross-section of the low-income population) suggest that there is a large pool of low-income homeowners who are interested in improving their property and are good credit risks. (3) Due to the Ministry of Housing and Land's (MOHL) strong promotion of rural (vs. urban) tenantry lots which are affordable for cash, the tenantry loan program proved unnecessary. Nonetheless, its objectives have been achieved. Also, many people used HI loan funds to purchase tenantry lots. TA was well justified, cost effective, and very instrumental in project success. A Housing Credit Fund (HCF) was established within the MOHL as implementing agency for the HG; the HCF is expected to have a long-term impact on housing policy (continued TA is recommended). The project also helped develop a National Housing Plan, computerized MOHL financial and research data, and provided other training/TA to credit unions, private builders and lenders, and other Barbadan staff. Moreover, the project gave commercial banks a positive experience which has led them to increase lending of their own funds to low-income borrowers, and also gave BMFC experience in lending to low-income homeowners, particularly those building chattel houses. Project design was suitably simple and implementation steady. Lessons learned are as follows: (1) government financial resources should be directed only at beneficiaries below a specified level, and subsidies only at those at the bottom of the income ladder; (2) except when the private sector will not build and housing is needed, the Government should focus on planning and on providing financial incentives to private builders, using a turnkey approach; (3) HI loans are an effective way to improve housing stock and move money through the private sector; (4) economic motivation can induce the private sector to enter a low-income market perceived as risky and less profitable; (5) constraints to expanding the role of the private sector in low-cost housing include not only financing, but also small downpayments, unavailability of small low-cost lots, and reluctance to build modest units.

Related documents