USAID FAMINE EARLY WARNING SYSTEMS NETWORK

Regional Maize Market Fundamentals

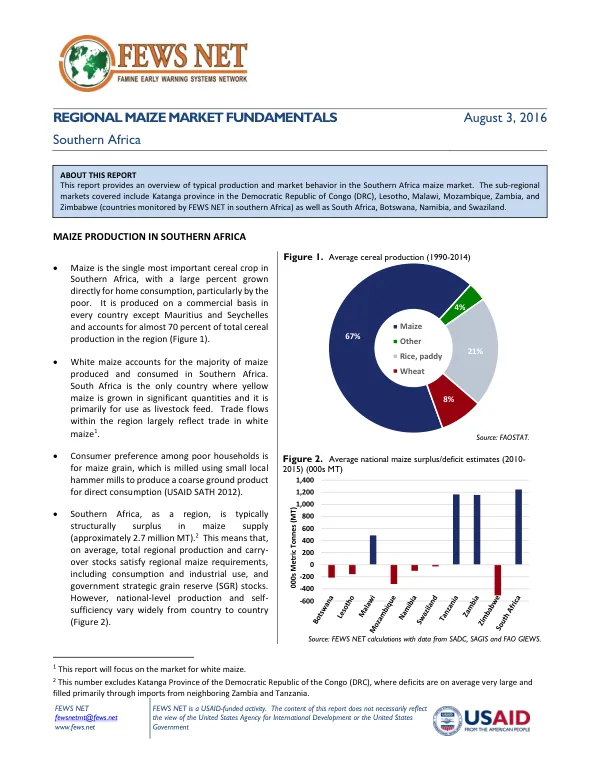

Maize is the single most important cereal crop in Southern Africa, with a large percentage grown directly for home consumption, particularly by the poor.

2016 · 4 pages

Sign in to readA free account is required to download.

Abstract

It is produced on a commercial basis in every country except Mauritius and Seychelles and accounts for almost 70 percent of total cereal production in the region. White maize accounts for the majority of maize produced and consumed in Southern Africa, with South Africa being the only country where yellow maize is grown in significant quantities and primarily for use as livestock feed. South Africa is the region's largest maize producer, contributing, on average, to over 40 percent of regional maize production. Although its domestic requirements far exceed those of other countries in the region, South Africa still typically produces a large exportable surplus of maize. South Africa exports, on average, 690,000 MT of maize to the region annually, making it the main source of maize supply for structurally-deficit countries in the region during average years. Zambia has become an important regional maize exporter, as local production has increased progressively. The region's dependence on rain-fed maize production has led to volatile output levels from one year to the next. Over the last 30 years, growth in maize production was mainly due to an increase in area under production. In general, South Africa, Tanzania, Zambia, and Malawi are countries that maintain a steady surplus while net deficit countries include Botswana, Lesotho, Namibia, Swaziland, Mozambique, and Zimbabwe. Trade flows across countries can be characterized by three main marketing basins, with the northernmost basin involving major trade flows from Zambia into the neighboring Katanga province and Malawi. The southernmost marketing basin includes trade flows from South Africa into Botswana, Lesotho, Mozambique, Namibia, Swaziland, and Zimbabwe. South Africa's maize industry has matured considerably following the emergence of major private trading companies and the launch of its commodity exchange, the South African Futures Exchange (SAFEX) in the late 1990s. South Africa has served as the main supplier for maize deficit countries in the region, and its maize production is largely from commercial farms. The third marketing basin involves significant maize flows from Zambia into Zimbabwe and Malawi. It also involves two-way trade flows between northern Mozambique and Malawi. Variations exist in per capita maize consumption across the region, with Lesotho, Malawi, South Africa, Zambia, and Zimbabwe all consuming relatively higher quantities of maize on a per capita basis. For a structurally deficit country like Lesotho, relatively high per capita maize consumption may be capturing other domestic requirements beyond human consumption, such as animal feed. There are various government agencies involved in maize marketing within the region, including the Agricultural Development and Marketing Corporation (ADMARC) in Malawi, the Grain Marketing Board (GMB) in Zimbabwe, the National Food Reserve Agency (NFRA) in Tanzania, and Zambia's Food Reserve Agency (FRA), which is one of the most influential maize marketing agencies in the region. FRA is a parastatal established to maintain national strategic food reserves and manage national storage facilities. As a major player in Zambia's maize market, the agency procures nearly all surplus maize at prices that typically exceed wholesale market prices in major maize-producing areas for either export or sale in the domestic market at pre-established prices.

Related documents