USAID. MISSION TO SWAZILAND

Swazi business development (SBD) project

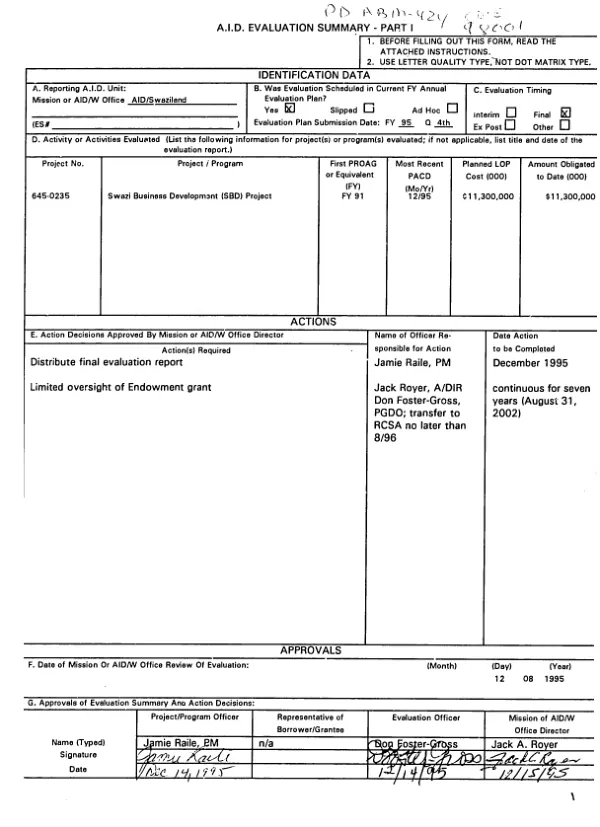

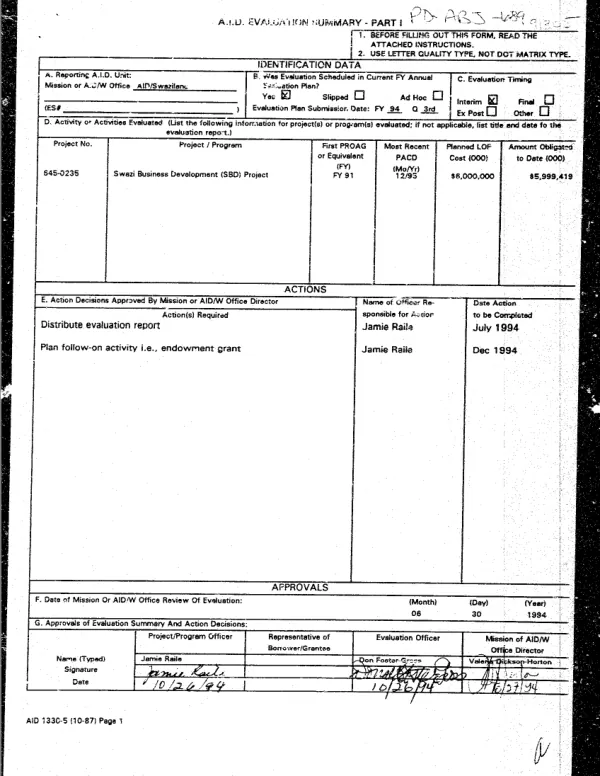

Summarizes final evaluation (PD-ABM-270) of a project (1991-12/95) to create the Swazi Business Growth Trust (SBGT) as a mechanism for stimulating the development of productive small businesses.

1995

Sign in to readA free account is required to download.

Abstract

The overall project impact has been positive; project indicators have been achieved or exceeded. Major outputs include: over 2,700 participants involved in SBGT training activities, over 1,300 loans issued to 505 first-time borrowers, and female entrepreneurs accounting for over 50% of the client base. The Class A lending program (small loans progressing in size) has been very effective in reaching first-time borrowers and in demonstrating the ultimate objective of helping those businesses to grow. Class A loan recipients have experienced growth in assets, profits, and/or employees; high repayment rates have occurred. However, the Class B lending program (larger, more traditional business loans), initiated in 1994, is experiencing delinquency problems and closer monitoring is called for. All Class A loan clients interviewed regarding the training provided by SBGT were enthusiastic -- most described it as "very good" or "excellent." Class B loan clients were generally less enthusiastic and believed that they needed more business training and follow-up assistance from SBGT. In the near to medium term, SBGT should solidify its programs and ensure a stable foundation for the long term before embarking in new directions. As SBGT solidifies its foundation, the issue of deposit taking should be reopened and reexamined with the Central Bank (SBGT is currently restricted from deposit taking). Deposit taking may be important for institutional sustainability as well as for serving client needs. The success of the project and the institution can be attributed to many factors including: the business-like nature of the institution, a private-sector oriented board and management, a proactive approach by SBGT in searching for business opportunities for small and medium Swazi businesses, and facilitation by the Government of Swaziland through the granting of a financial institution license, access to a low-interest rate loan, and participation in various SBGT sponsored events. The following lessons were learned. (1) More effort than is generally assumed may be needed to educate the public, potential borrowers, and government officials about lending to micro, small and medium enterprises, especially the need for charging interest rates which allow for institutional sustainability, and that this interest rate is generally more than commercial banks charge. (2) Education is just as important as credit -- understanding cash flow management, pricing, and other business principles makes a critical difference in entrepreneurial success. (3) With the necessary resources and community support, it is possible to develop a small business support institution in a relatively short period of time that allows for expected sustainability in the medium term. (Author abstract, modified)

Related documents

![Project assistance completion report : business management extension program (BMEP)/LULOTE [luhlelo lolunotsisa temabhizinisi (program for business development)]](https://covers.devme.ai/gen/6702.webp)