USAID DEC

Financing Options for Natural Resource Products in Community Resource Management Areas

Sign inFEED THE FUTURE

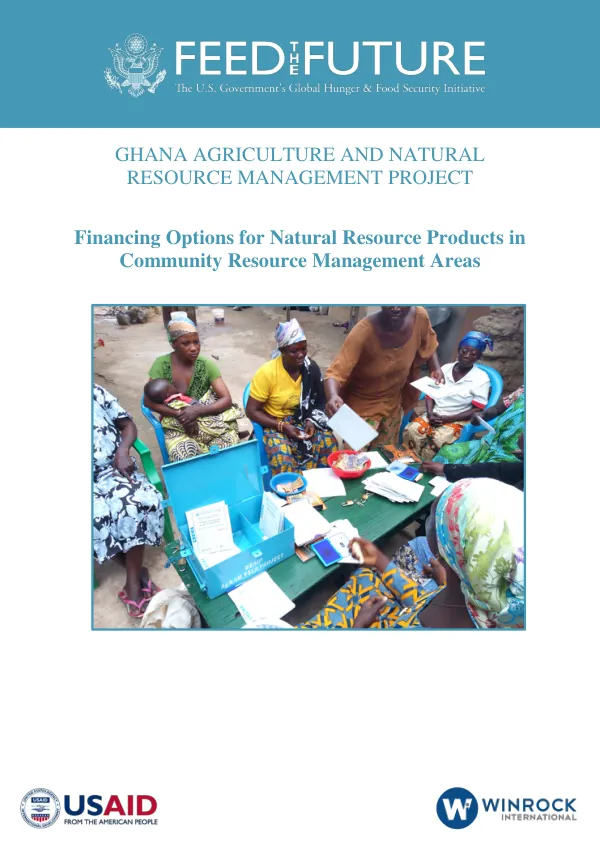

Financing Options for Natural Resource Products in Community Resource Management Areas

The Ghana Agriculture and Natural Resource Management Project aims to improve the livelihoods of rural communities through the development of natural resource products (NRPs).

2018 · 32 pages

Sign in to readA free account is required to download.

Abstract

NRPs contribute significantly to rural livelihoods, with 38 percent of Ghanaian households engaging in the NRP trade, thereby increasing their household incomes by 20 percent. The predominant NRPs in northern Ghana include shea, moringa, dawadawa, tamarind, and baobab. However, collectors and producers of NRPs struggle with access to markets and the technical know-how to produce at the required quality level. Many smallholders also face difficulties in accessing financing that would allow them to upscale their operations in terms of agricultural inputs, raw materials, small production tools, and larger production assets. Formal financial institutions, such as private banks or rural and commercial banks, are often located too far from rural communities and frequently unable to provide financing options that are within the means of smallholders. The situation is worse for women, who face additional cultural barriers and lack access to collateral due to land tenure norms in Ghana. As a result, NRP collectors and producers in the Community Resource Management Areas (CREMAs) often resort to more informal mechanisms to finance their operations, such as village savings and loan associations (VSLAs). VSLAs offer more flexible, timely, and accessible financing options than formal financial institutions, but the loan amounts they provide to members are mostly insufficient for business expansion. The report highlights the strengths and weaknesses of financial options available to NRP groups in the CREMAs. Formal financial institutions, such as private banks and rural and commercial banks, offer large loan amounts and longer term repayment periods, but are often perceived as having high interest rates and complex application procedures. Semi-formal institutions, such as NGOs and microfinance institutions, also offer large loan amounts and longer term repayment periods, but are perceived as having high interest rates and lack of focus on NRP businesses. Informal institutions, such as VSLAs, offer low interest rates and flexible repayment terms, but have small loan amounts and are not professionally managed. The report concludes that there is a need for more accessible and affordable financing options for NRP collectors and producers in the CREMAs. Building on kinship ties and social solidarity, VSLAs offer a promising approach to providing financing options that are within the means of smallholders. However, there is a need for further research and development to improve the efficiency and effectiveness of VSLAs in providing financing options for NRP collectors and producers. The report also highlights the importance of addressing the cultural and social barriers that prevent women from accessing financing options. Women face additional cultural barriers and lack access to collateral due to land tenure norms in Ghana, making it difficult for them to access financing options. Addressing these barriers is critical to improving the livelihoods of rural communities and promoting economic development in Ghana. In terms of implementation, the report recommends that financial institutions and development organizations work together to develop more accessible and affordable financing options for NRP collectors and producers in the CREMAs. This could involve providing training and capacity-building programs for VSLAs and other informal institutions, as well as developing new financial products and services that are tailored to the needs of NRP collectors and producers. The report also recommends that policymakers and development organizations address the cultural and social barriers that prevent women from accessing financing options. This could involve implementing policies and programs that promote women's access to land and other forms of collateral, as well as providing training and capacity-building programs for women to improve their financial literacy and management skills. Overall, the report highlights the importance of improving access to financing options for NRP collectors and producers in the CREMAs. By addressing the cultural and social barriers that prevent women from accessing financing options and developing more accessible and affordable financing options, policymakers and development organizations can promote economic development and improve the livelihoods of rural communities in Ghana.

Related documents