UNITED NATIONS

Health Insurance Profile: Ghana

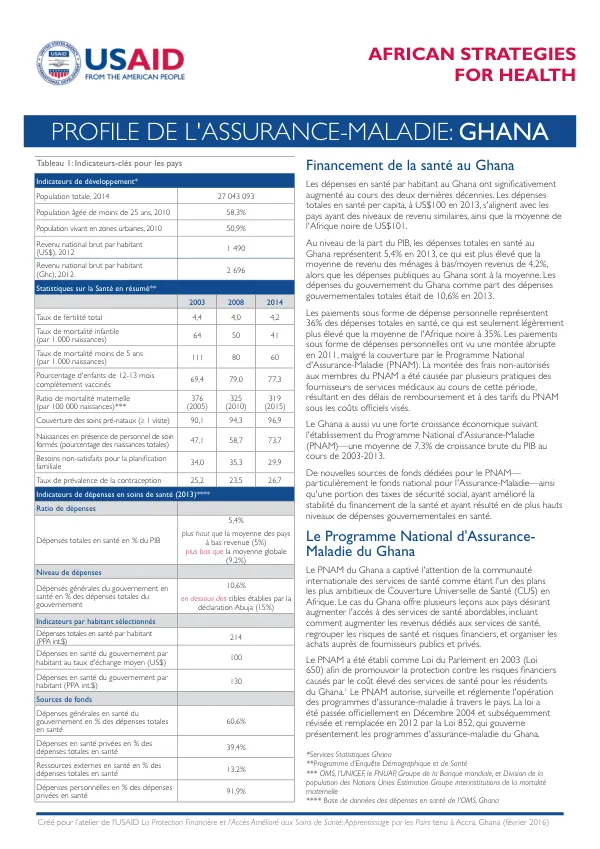

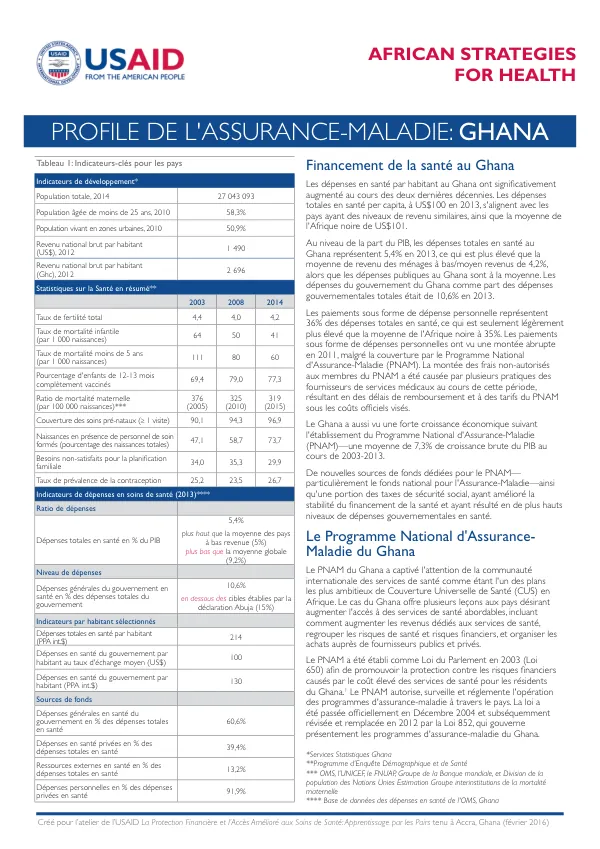

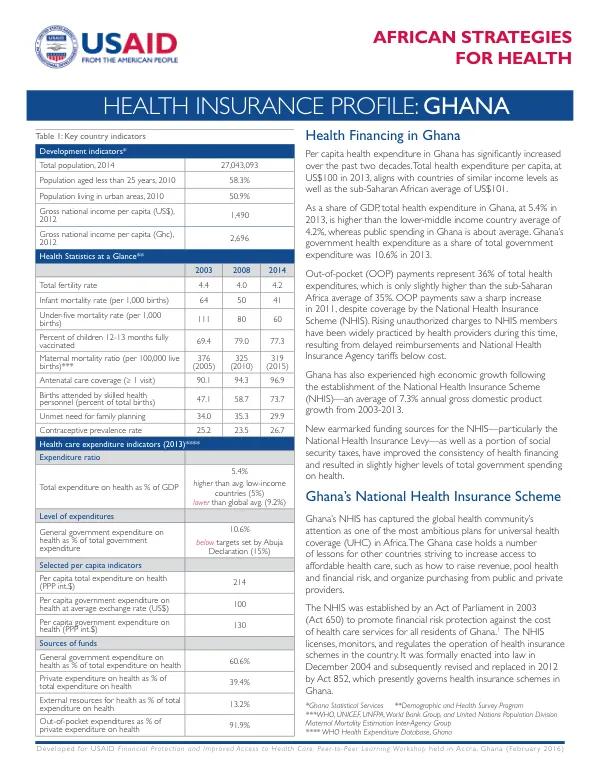

The National Health Insurance Scheme (NHIS) in Ghana was established by an Act of Parliament in 2003 to promote financial risk protection against the cost of healthcare services for all residents of Ghana.

2016 · 4 pages

Sign in to readA free account is required to download.

Abstract

The NHIS licenses, monitors, and regulates the operation of health insurance schemes in the country. It was formally enacted into law in December 2004 and subsequently revised and replaced in 2012 by Act 852, which presently governs health insurance schemes in Ghana. The NHIS is governed by the National Health Insurance Authority (NHIA), a centralized government agency with headquarters in Accra. Act 852 established a unitary scheme with offices throughout the country, including a Head Office, Regional Offices, and District Offices. The NHIA accredits public and private providers and is responsible for policy and overall operations of the NHIS. The NHIS is financed on a national basis from a single National Health Insurance Fund (NHIF), a pool for the sharing of health and financial risk. All funds are channeled through the NHIS. The main source of financing is the VAT-based National Health Insurance Levy (2.5% VAT). Earmarked funds constitute over 90% of total inflows; over 70% derive from the NHI levy and roughly 20% from contributions made by formal sector workers to the Social Security and National Trust (SSNIT). An additional 10% comes from other sources, including premium payments. The NHIS has a nationally standardized and comprehensive benefits package, intended to cover 95% of disease conditions and includes primary, tertiary, and pharmaceutical goods and services. NHIS enrollees may access benefits at NHIA-accredited public and private providers; members must first report to a primary care facility, and subsequently to second and third levels of care by way of referral. Exemption from copayments or fees at the point of service is mandated by law but not enforced in practice. The minimum benefits package includes general outpatient and in-patient care, oral health, eye care, comprehensive delivery care, diagnostic tests, generic medicines, and emergency care. The NHIS maintains an exclusion list of health problems, including cancer treatment other than breast and cervical cancers, dialysis for chronic renal failure, organ transplants, and services provided under government vertical programs, among other tertiary services. Female reproductive health is emphasized in the benefits package, with benefits for maternity care including antenatal care, caesarean sections, and postnatal care for up to six months after birth. A 2015 study examined the extent to which the NHIS protects its members against the financial consequences of ill health. Results showed that the insured were more likely to seek health care and also had significantly lower out-of-pocket payments compared to the uninsured. Another 2015 study on the effect of insurance enrollment on maternal and child health care found that the likelihood of seeking formal medical care and fever treatment is higher among the insured. When a fever or cough has been reported for a child, NHIS coverage increases the likelihood of seeking formal medical treatment by 65.5 percent and increases the likelihood of receiving malaria medication by 71.8 percent. The NHIS has not completely eliminated catastrophic health expenditures among its members, but it provides significant financial protection in times of ill health for insured households. This is consistent with the general observation that the NHIS is making positive impacts on reducing the financial barriers to health care in Ghana.

Related documents