USAID

Ministry Evaluation Scoring Matrix

The Ministry Evaluation Scoring Matrix assesses the performance of various ministries in the country.

2016 · 10 pages

Sign in to readA free account is required to download.

Abstract

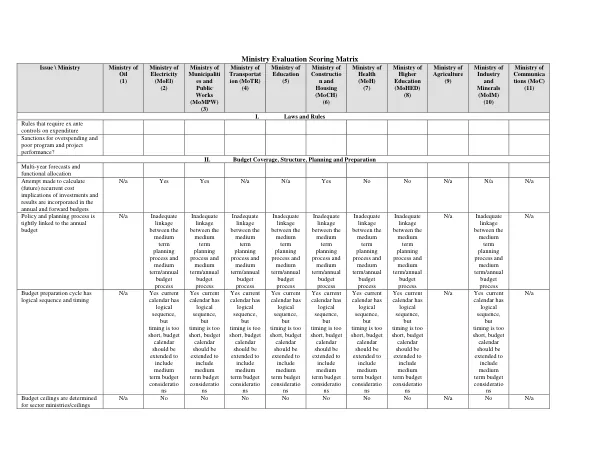

The evaluation focuses on several key areas, including laws and rules, budget coverage, structure, planning, and preparation, budget execution, and accounting subsystems. In terms of laws and rules, the evaluation reveals that some ministries have rules that require ex ante controls on expenditure, while others do not. Sanctions for overspending and poor program and project performance are also not consistently applied across ministries. The Ministry of Finance (MoF) provides final budget ceilings after ongoing discussions with sector ministries. The evaluation also examines budget coverage, structure, planning, and preparation. Multi-year forecasts and functional allocation are not consistently used across ministries, and some ministries have inadequate linkage between the medium-term planning process and the medium-term/annual budget process. However, the current budget calendar has a logical sequence, but the timing is too short, and the budget calendar should be extended to include medium-term budget considerations. In terms of budget execution, decentralized payments do not undermine expenditure control in some ministries, while others have centralized control structures. Information on actual expenditure is available on time for monitoring tasks in some ministries, but others have inadequate cash flow analysis and use of integrated Financial Management Information Systems (FMIS). The evaluation also assesses the effectiveness of internal controls for non-salary payments, expenditure commitment controls, and other internal control rules and procedures. Some ministries have unclear compliance with rules for processing and recording transactions, while others have control rules and procedures not well documented. The evaluation also examines the availability of data for monitoring the stock of expenditure payment arrears and the payment system. Some ministries have centralized payment systems and make payments on time, while others have inadequate data for monitoring payment arrears. In terms of the accounting subsystem, the evaluation reveals that accounting and budget classification are not fully integrated into a single common classification in some ministries. Some ministries follow the current budget coding structure but are not in complete compliance with the Government Finance Statistics (GFS) 2001. Overall, the evaluation highlights areas of strength and weakness across various ministries, providing a comprehensive assessment of their performance in key areas.

Related documents