USAID

The Executive's Internal Control Pocket Reference

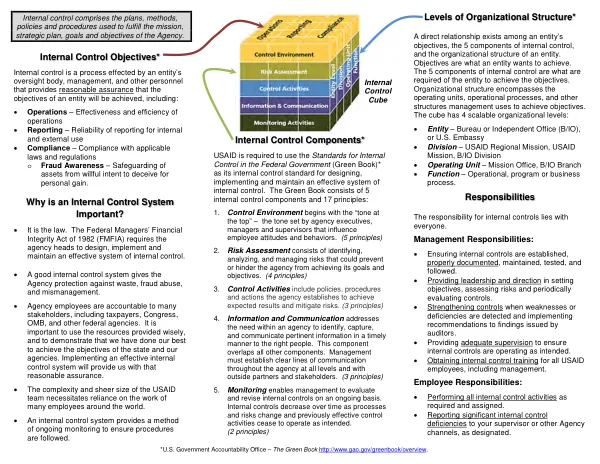

The Green Book, a comprehensive guide to internal control, is a cornerstone of the U.S.

2016 · 2 pages

Sign in to readA free account is required to download.

Abstract

Government Accountability Office's (GAO) Standards for Internal Control in the Federal Government. The document outlines the importance of internal control in achieving an entity's objectives, ensuring the effectiveness and efficiency of operations, and providing reasonable assurance that the entity's financial statements are accurate and reliable. Internal control is a process that involves the plans, methods, policies, and procedures that an entity's oversight body, management, and other personnel use to fulfill its mission, strategic plan, and objectives. The Green Book identifies five components of internal control: Control Environment, Risk Assessment, Control Activities, Information and Communication, and Monitoring. The Control Environment component sets the tone at the top, demonstrating commitment to integrity and ethical values, exercising oversight responsibility, establishing structure, responsibility, and authority, and enforcing accountability. The Risk Assessment component involves identifying, analyzing, and responding to risks that could hinder the entity's goals and objectives. The Control Activities component includes policies, procedures, and actions that the entity establishes to achieve expected results and mitigate risks. The Information and Communication component requires the entity to identify, capture, and communicate pertinent information in a timely manner to the right people. The Monitoring component involves evaluating internal controls on an ongoing basis to ensure they are operating as intended. The Green Book also emphasizes the importance of employees at every level in internal control, as they are responsible for performing internal control activities and reporting significant deficiencies to management. Effective internal control helps the entity achieve its operations, reporting, and compliance objectives. The Federal Managers' Financial Integrity Act (FMFIA) requires agency heads to annually submit a statement of assurance regarding the adequacy of internal control. The statement must take one of three forms: a modified statement of assurance, a statement of assurance, or a statement of no assurance. The FMFIA also requires a separate report on whether the agency's financial systems comply with government-wide requirements. The Green Book is a comprehensive guide to internal control, providing a framework for entities to establish and maintain effective internal control systems. By following the Green Book's guidelines, entities can ensure the accuracy and reliability of their financial statements, achieve their objectives, and provide reasonable assurance that their internal control systems are operating as intended. The Green Book's five components of internal control are essential for achieving an entity's objectives. The Control Environment component sets the tone at the top, demonstrating commitment to integrity and ethical values. The Risk Assessment component involves identifying, analyzing, and responding to risks that could hinder the entity's goals and objectives. Effective internal control is essential for achieving an entity's objectives, ensuring the effectiveness and efficiency of operations, and providing reasonable assurance that the entity's financial statements are accurate and reliable. The Green Book provides a comprehensive guide to internal control, providing a framework for entities to establish and maintain effective internal control systems. The Green Book's emphasis on employees at every level in internal control is crucial for achieving an entity's objectives. Employees are responsible for performing internal control activities and reporting significant deficiencies to management. Effective internal control helps the entity achieve its operations, reporting, and compliance objectives. The Green Book's emphasis on employees at every level in internal control is crucial for achieving an